By David Arbit on Monday, April 17th, 2017

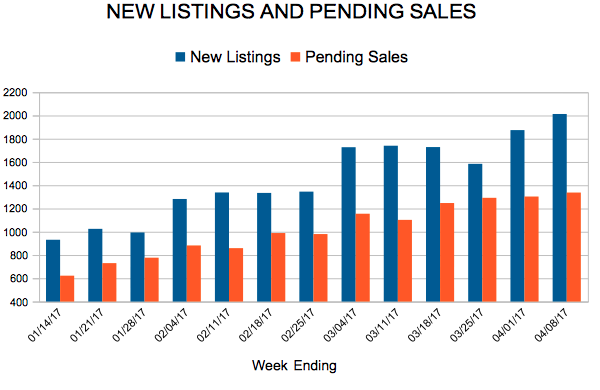

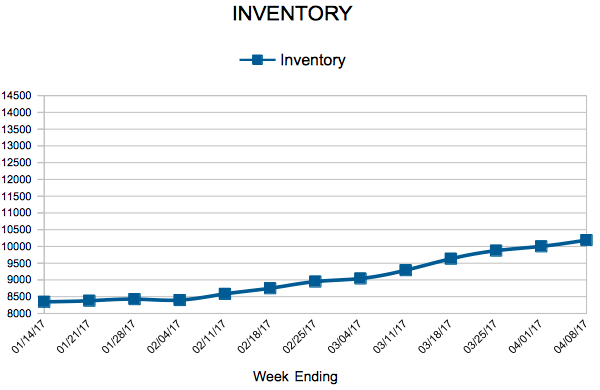

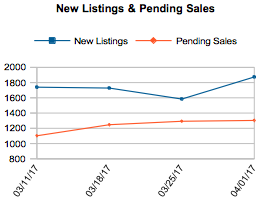

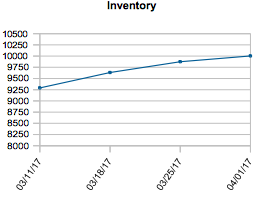

Seller activity rose 1.3 percent compared to March 2016. The number of signed purchase agreements declined 3.0 percent, though the number of closed sales rose 8.3 percent. Housing demand has outpaced supply, thus continuing the trend of falling active listings. In March, inventory levels fell about 20.0 percent compared to 2016 levels. Those shopping for homes have 10,213 properties from which to choose in the metro area. Given that figure stands near a 15-year low and demand has reached an 11-year high, affordably-priced homes that are listed often fetch full-price offers or better in record time.

These market conditions tend to drive prices higher. The median sales price increased 7.0 percent from last March to $237,500. Multiple offers on attractive, turn-key properties in the most desirable neighborhoods and school districts are common in low inventory environments. Properties also tend to sell quickly and for close to or above list price. Average days on market until sale fell 14.1 percent to 73 days compared to 85 in March 2016. It’s worth noting that the median days on market for March was a brisk 34 days. The average percent of original list price received at sale was 98.1 percent, 1.3 percent higher than last March. Similarly, the median percent of last list price received at sale was 100.0 percent. The Twin Cities has only 2.0 months of housing supply—the lowest March reading since 2003. Generally, five to six months of supply is considered a balanced market where neither buyers nor sellers have a clear advantage.

“Buyers were still very active during the first quarter,” said Cotty Lowry, Minneapolis Area Association of REALTORS® (MAAR) President. “This is encouraging as households adjust to marginally higher borrowing costs, though it’s likely a lack of listings that’s suppressing even stronger gains.”

A thriving local economy has been conducive to housing recovery. The most recent national unemployment rate is 4.5 percent, though it’s 4.2 percent locally. The Minneapolis–St. Paul region has a diversified and resilient economy with a talented workforce that’s enabled one of the highest homeownership rates in the country.

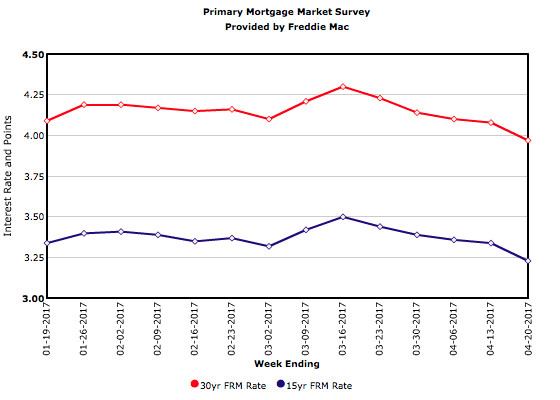

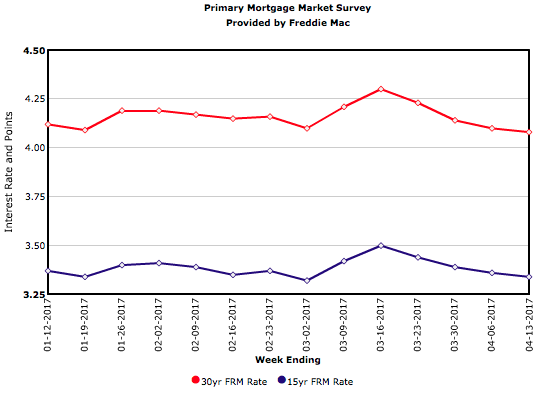

The average 30-year fixed mortgage rate has declined from 4.3 percent to 4.1 percent lately, still well below a long-term average of about 8.0 percent. Barring any unforeseen events, the Federal Reserve is likely to increase their target federal funds rate at least once more this year. Wage and inventory growth are key to offsetting affordability declines brought on by higher rates.

“We’re still seeking a healthier balance in the marketplace that enables all participants to achieve their goals,” said Kath Hammerseng, MAAR President-Elect. “It’s essential to bring additional options to buyers, particularly in the more affordable price brackets.”

From The Skinny Blog.